When you don’t have enough money, it can seem like the most basic monthly costs can be challenging to manage and induce stress. For many households, money can be tight to the point that at the end of the month, you are juggling rent, electricity, food, transportation, etc. Money issues are not only about avoiding or coming up with a plan when you do not have enough cash to survive the month, but also about developing financial habits to help you achieve your monthly obligations.

Money issues are not uncommon; most families are underreported because they have so many stigmas associated with them. Not many people can admit to living paycheck to paycheck and being stressed or overwhelmed by unplanned or unexpected expenses. With the following strategies, moving forward, you will understand tactics such as prioritizing your bills and handling financial stress, and you will receive beneficial tips to help you pay your bills.

This article will provide helpful steps for staying organized and reducing bill late fees while dealing with limited income and financial stress.

When money is tight, it's easy to feel like there is never enough. Rent or mortgage payments may consume a significant portion of the income, not to mention all the utility bills, transportation expenses, and food costs. Problems escalate when you face unexpected medical bills, car repairs, and debt payments that you didn't plan to have to make.

Living on a low income sometimes leads to anxiety; however, when you add a lack of organization, it can make matters worse. Missed due dates lead to late fees and higher interest charges that can stretch a limited budget. By learning to organize payments and to recognize priorities, you begin to experience a clear path that can help reduce stress.

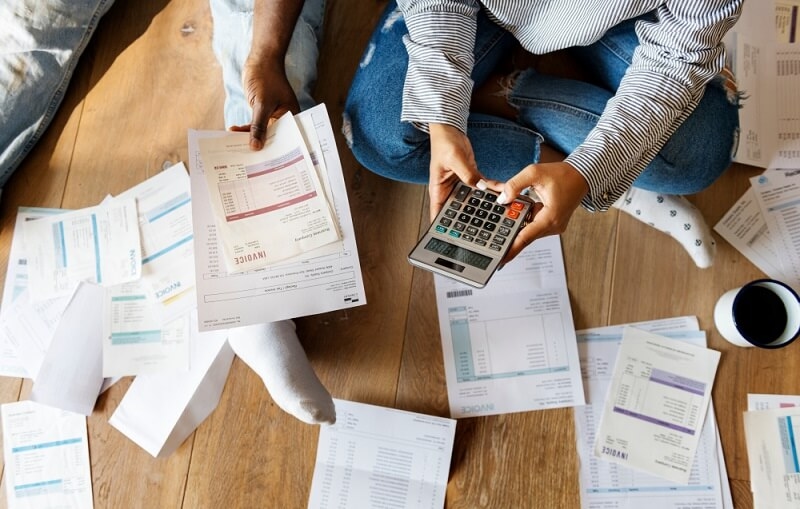

The initial action in bill management for those with low income is to take stock of their overall financial circumstances. Ignoring them will not make them disappear.

This simple method allows you to see where your money is going, forcing you to identify where you can start to cut back.

Not every bill is created equal. When money is tight, you must assess what payments mean the most to your stability and safety.

Following this order helps minimize the risk of losing your home, having your utilities cut off, and being unable to get to work or school.

Being organized is half the battle. One of the best payment tips is keeping a due date calendar.

Having a calendar lessens stress by allowing you to feel good knowing nothing is getting missed.

You may need to make sacrifices when managing bills with a limited income. This doesn't mean losing out on some happiness—it means tightening up for a short while.

Every little reduction opens up extra money for essentials.

Many people don’t realize that bills aren’t always set in stone. If you’re struggling, call your service providers and explain your situation.

I want you to know that being proactive shows responsibility and may keep your accounts in good standing.

Sometimes, managing bills requires seeking outside help. This is not a sign of failure—it’s a step toward survival and rebuilding.

Use these resources as temporary tools to stabilize your finances while working on longer-term strategies.

For people who forget due dates, having automatic payments for specific bills means you don't have to worry about late fees. Although particular costs may be trivial, they add up fast, as do missed payments. We've all seen the stories about how missed bills and expenses can damage your credit score.

For bills you cannot set up automation for, you could always set aside the funds and put them in separate envelopes or accounts until the payment is made.

When every dollar matters, budgeting is critical. Two effective strategies include:

These approaches prevent overspending and keep you focused on priorities.

When money is tight, payday loans might seem tempting. But these are traps that make financial struggles worse.

Instead of borrowing from predatory lenders, consider:

Protect yourself from cycles of debt by avoiding high-interest quick fixes.

Debt payments can squeeze your budget and make it hard to pay for necessities. While paying everything off all at once may not be possible, you can start small.

By paying off debts to free up your monthly cash flow, you will, over time, have lower monthly payments and greater breathing room.

When struggling with bills, avoid these pitfalls:

Being aware of these mistakes helps you make more intelligent choices.

Learning to manage bills when money is tight is essential and requires patience, organization, and perseverance. By facing your financial situation directly, using best practices in paying bills, and making hard decisions, you can reduce your difficulty in managing your bills, feel less stressed, avoid late penalties, and get by on a limited income.

Key points: Identify and focus on basic priorities; get help when needed; develop a habit of setting and obtaining long-term security. Financial distress does not define you; it is only a circumstance that can be overcome with effort and planning.

This content was created by AI